If you’re like me and passionately roll up your sleeves and get to work on something great for several years or more (your business), you owe it to yourself to have a final result for your efforts that is truly a masterpiece.

I’m talking about your business, once it’s complete…Done…Ready to sell for as much as you can reasonably expect, often for several times its yearly earnings.

If and when it does come time to sell, you want to be selling from a position of strength-to sell it when it is at its most valuable point and not when you’re burned out, in ill health, or in some other situation where you are rushed or won’t make nearly as much from the sale.

Like any great work, you have to start with the end in mind, and to that end I’ll be writing this to clarify just what a “sellable” business looks like. This will give you an ideal to work towards and guide your plans and work.

Below are several things to be aware of in increasing the value of your business to yourself and potential acquirers.

Positioned in its clearly-defined niche

Your business must be the best it can be at what it does, without trying to be everything to everyone. A business that knows its customer segments, their needs and language, and how to solicit a response from them is a lot more valuable than one that is a mixture of everything, or an unknown in its market.

Coach your team to run the business without you

Could other people ever run your business without you? They’ll have to, if you’re selling! So why not make this your goal from Day One?

Make an organizational chart of how your business will look when it’s time to sell it. List all the various workers in marketing, operations, and those they report to. It’s okay if it’s just you or a handful of people currently filling all those roles. Doing this will help you organize who is going to do what in your business before you hire a new person.

Then, over time, you can find other people to fill those positions one by one until you’re out of the picture.

Build relationships with customers

Goodwill, such as your reputation and brand in the minds of your current and prospective customers, is considered an asset on your company’s balance sheet. You build this over time by treating people right and maintaining good relationships.

If you intend to sell your business someday, or if you just want to have the option, this is something you have to make a priority throughout the business’s life. You can’t just start doing it well suddenly in the final year. Relationships and recognition take time.

Make sure you’re stable

Make sure you’re not overly dependent on any one customer, vendor, employee, or anything else. Diversify your strengths. If you have any “whale” customers that make up a large portion of your business, try to get at least 80% of your business from other people.

The new owner does not want to take the reins and have revenues drop in half in the event your biggest customer leaves.

Maximize your revenues

This one’s self-evident, but deserves to be repeated. In my last essay, I shared 4 proven ways to increase your revenues-getting more customers, increasing your average order size, get customers to buy more frequently, and finding new ways to monetize your customers and visitors.

A company with higher revenues and which shows growing revenues will be more valuable and attractive to buyers.

Hold expenses accountable

You boost your net profit (and therefore the value) by reducing your expenses. However, no one ever shrank themselves into wealth. You’re not going to grow your business by keeping expenses lower-but the numbers will increase as it grows.

Your goal is to keep the percentages the same, such as keeping advertising at 20% of your revenues whether earnings are $100,000 or $1,000,000 per year.

Basically, you’ll want to make sure that budgets are made and followed, to keep spending within projected limits and to avoid costs creeping up that don’t generate more revenue in return.

Keep great records for the next owner

Keep excellent records of everything for the new owner-your files, databases, customer communications, marketing materials, financial records, employee agreements-everything.

Committing to do this now will make your life so much easier between now and the time you sell. Keep good records for your own efficiency, protection, and to make your business look a lot more attractive to buyers than one where all the records are filed away in the old owner’s head.

Develop a plan for when it’s “done” and ready to sell

I don’t want you to have plans on top of plans, but each of these will take certain actions to make them happen. So here’s what to do: Add these end results into your existing business plan, and use your best judgment when choosing how to make each of them happen in your company.

When it’s all said and done, the next few years are going to go by whether you maximize your business’s value or not. At the end of, say, 5 years, would you rather have a stable, attractive, polished business ready to sell for top dollar, or be left taking what you can get for what you have?

If it seems like a lot, remember you have until the time you sell to take care of these things. You don’t have to do it all now! Just add these elements I described to your vision of what you want your company to be, and keep your eye on it until the big day finally comes.

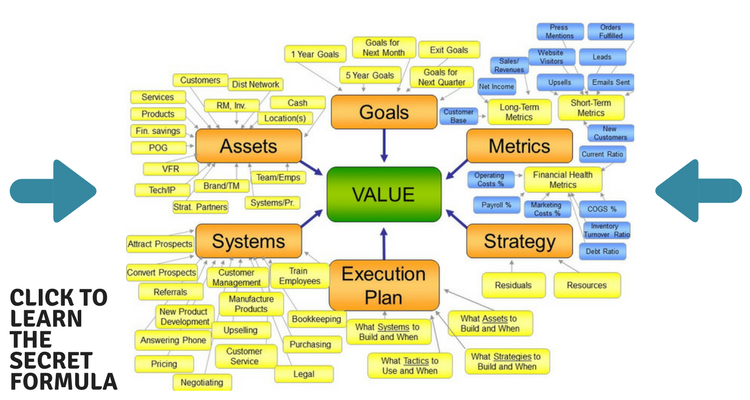

The Secret Formula to

Building a $10 Million Company

If you want to build a $10 million+ company, you must focus on building Value. And to build Value, you need to follow a specific formula.

On this page, I layout the precise formula for you.

As you scroll down the page, you’ll see the important schematic below:

Don’t be overwhelmed by its complexity, by the time you see it, it’ll make perfect sense. And you’ll be able to follow it to dramatically grow your business.

Click here to learn how to grow a $10 million+ company today